Skinny: Before buying an LIC policy, here are some critical, mind-bending facts which you need to know. In a way this is also everything that your agent doesn’t want you to know.

The golden rule to not mix insurance and investment is now an old one. You’ll always be better off buying a pure term policy for life insurance, and investing the rest into mutual funds(equity or debt – depending on your goals).

This post isn’t about the low overall effectiveness of such an LIC policy, but about your hard earned wealth which ends up working for your LIC agent.

This is not a review of term life insurance policies, but of ‘whole life plans, ‘pension plans’, ‘endowment plans’ etc. These are typically advertised as tax-saving life insurance products which also provide a return.

WHAT’S THE FUSS ABOUT?

Sales commissions. The fuss is about sales commissions in an LIC policy.

Buying an LIC policy rewards your angent handsomely. He/she basically receive a percentage of your payments as income. Not just once, but for as long as you are making your payments. Which basically means you become your agent’s source of income.

A sales commission might sound fair. Without commissions no one would have an incentive to sell anything after all. The problem though is two fold.

- The size of these commissions.

- The fact that this is your money, working for someone else, without your notice.

WHAT PERCENTAGE IS PAID AS COMMISSIONS IN AN LIC POLICY?

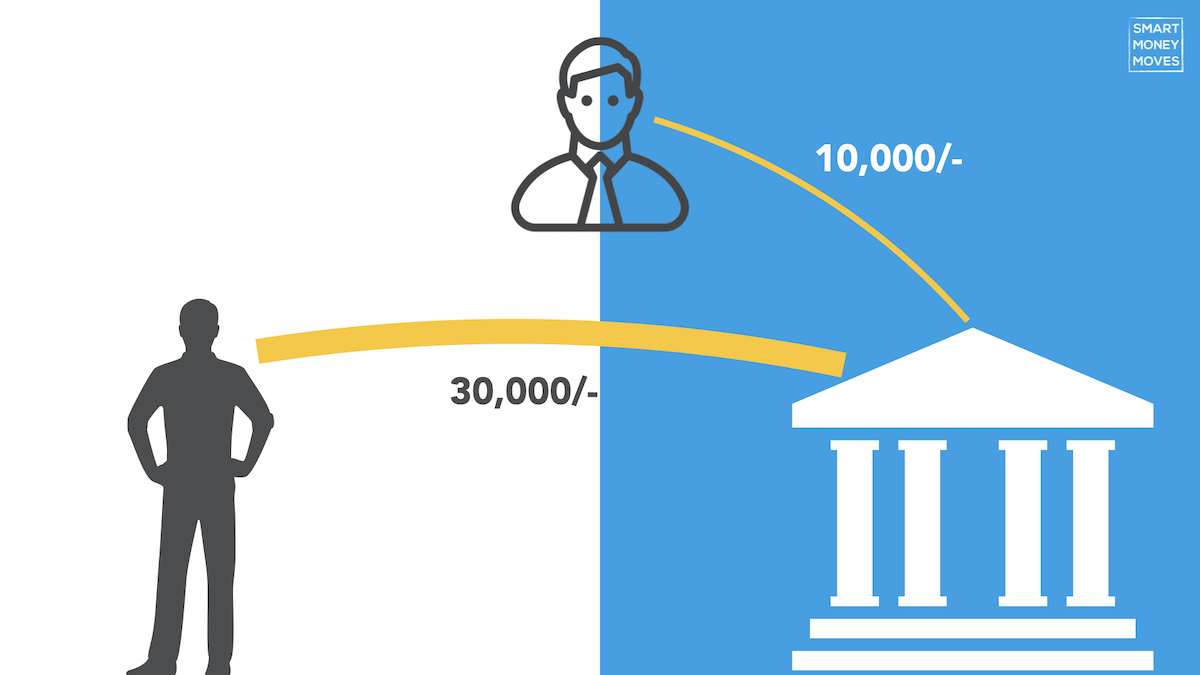

The first year

Anything between 25 to 35% of you’ve paid will be paid to your agent as commission.

As an example:

- If you were to pay a premium of 30,000/- per year, anything from 7500/- to 10,000/- would go straight to your agent.

- If you were to pay a premium of 1,00,000/- per year, anything from 25,000/- to 35000/- would go to your agent.

For every year after

- Your agent could receive anything from 5 to 10% as commission.

- He/she receives it as long as you are paying premiums – which could easily span decades.

Then there bonus commissions in LIC policies

Some policies also provide agents with an additional ‘bonus commission’ of 40% in the first year.

[Source: JoinLICIndia]

Do agents disclose LIC policy commissions to their clients?

Nope. If they did, no one would willingly buy a policy from them.

Buying

HOW SEVERE IS THE PROBLEM OF AN AGENT MISSELLING AN LIC POLICY?

Pretty severe. Returns and benefits are often glorified and have no correlation to actuals. Even well educated individuals fall prey to this mis-selling since most folks lack a necessary understanding of finances. In reality, most LIC policies barely provide a return of 2-3%, with perhaps a tiny handful providing 5-6%.

So yes, the problem is rather severe.

1. LIC encourages its agents to ‘convert their contacts into cash’

I’ve come across several cases where the misselling was done by a person’s relative, colleague, a neighbor, and at times even a sibling. Folks often find it hard to say no to them, on account of having a personal connection.

2. So rampant, that Harvard Business School did a study on it

The problem is so rampant, that Harvard Business School even did a 4-year study on it, and concluded that rampant mis-selling occurs in the Indian insurance space – and that agents often recommend insurance products which bring them more commissions, rather than what’s good for their clients.

I’ve written extensively about these commissions in my last post on ULIPS – which are also products which should be completely avoided.

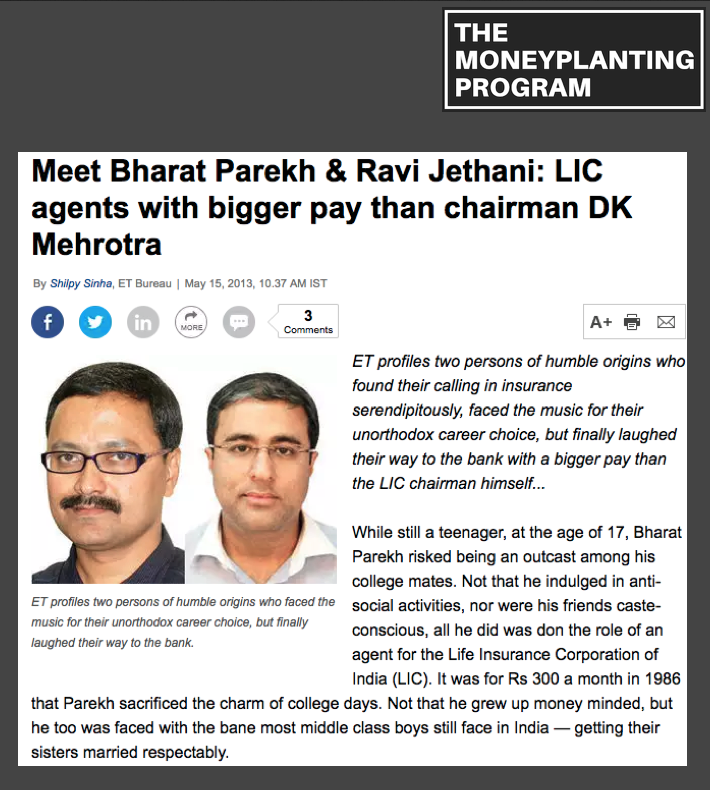

3. So rampant, that it’s made some agents ridiculously rich

This is the snapshot of an article which made rounds in 2013. A couple of LIC agents were making more in commissions, than even the chairman of LIC.

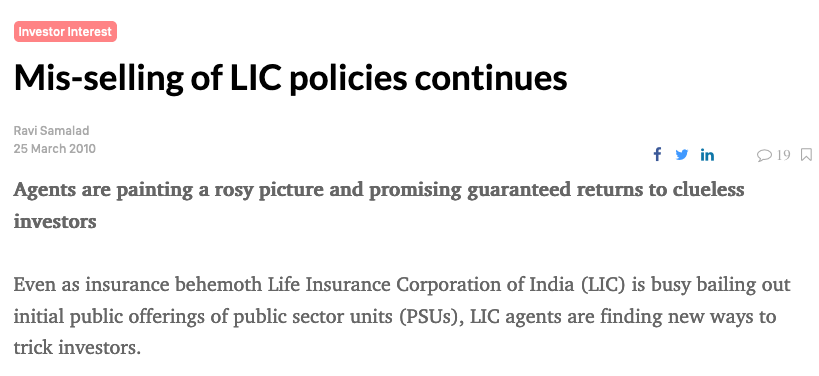

4. So rampant, that its easy to find articles like these

This article is from Moneylife – another portal which genuinely cares about investor’s interests.

How to exit if you’ve already invested in a LIC policy?

Unfortunately, Every LIC policy and ULIP is different. So a blanket recommendation on when or how to exit is impossible to make. Start first by calling your agent or customer care and asking what would happen if you did exit.

It’s highly likely that you may still not get transparent, honest answers. There are now reports of agents telling their clients that they cannot even withdraw their matured policies and the proceeds will need to be invested into another policy. That is a level of mis-selling that is shocking to hear. But, not surprising.

I’d suggest building up some basic knowledge of investing, so you can take a decision. If you think you’re not up for it, you can consult a fee-only financial advisor.

Conclusion: Should you invest in an LIC policy?

As an investor, you should avoid buying an LIC policy which provide a mix of both insurance and investment. Such policies are sold by several other entities as well. They can all be comfortably avoided.

Most LIC agents will refuse to sell you a pure term insurance policy if you don’t buy any of their whole-life or endowment policies. This is because commissions they get in pure term policies are significantly low. But the fact is that the only type of life insurance cover you need, is a term life insurance.

[ Get posts like these delivered to your inbox. No ads. Ever. ]

Good luck.

Vinod

A beginner’s book on investing unlike any other

Learn everything a working adult needs to know about money and investing

From bare bones fundamentals, and to a solid 10-year head start. All taught in a way never taught before.